The Silent Score Killers: Common CIBIL Errors Borrowers Never Notice | Lawfully Finance

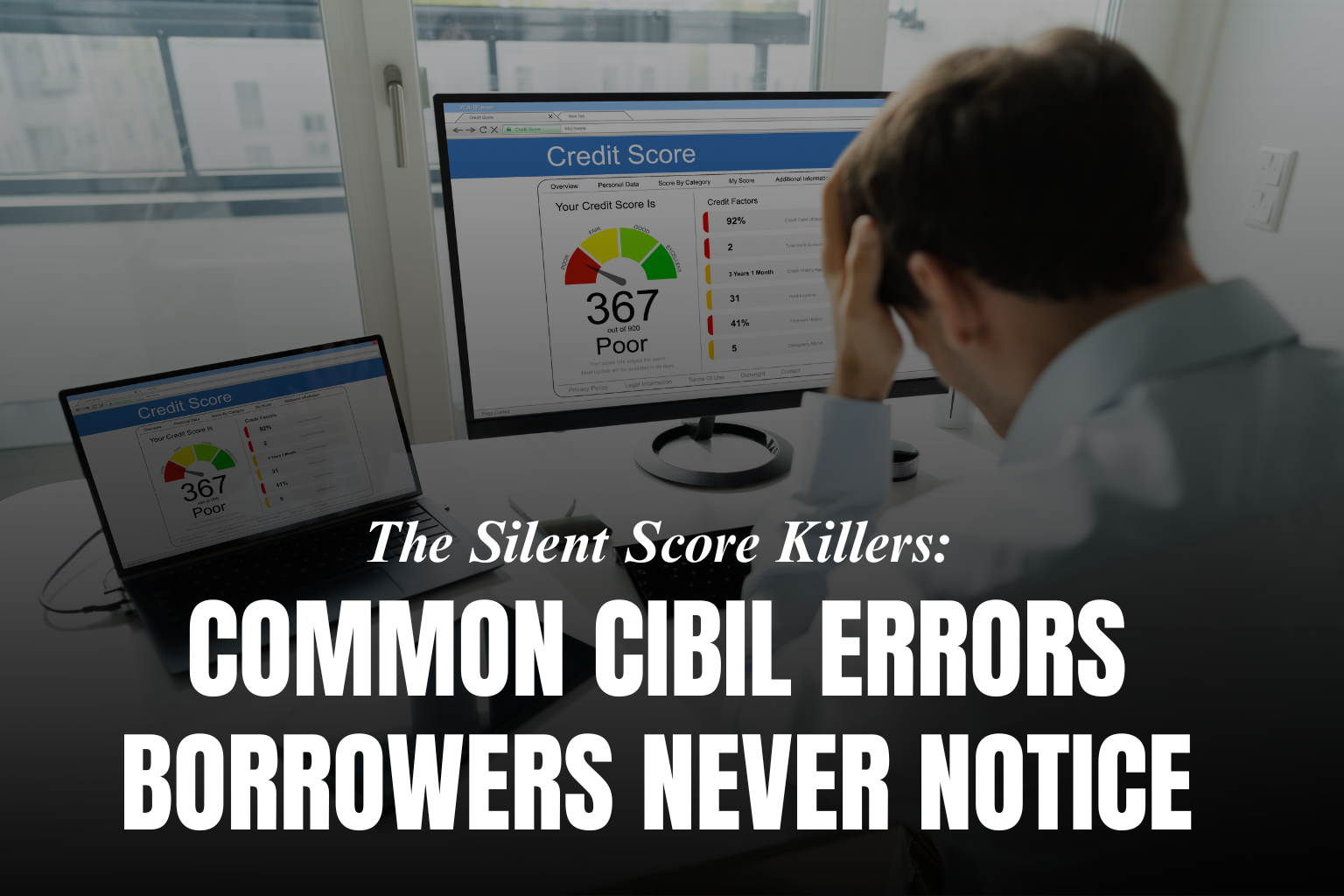

Many borrowers blame missed EMIs or past settlements when their CIBIL score drops. While those factors matter, a surprising number of low scores are caused by silent errors—mistakes in credit reports that borrowers never notice until a loan is rejected. These errors quietly damage creditworthiness, limit options, and raise borrowing costs.

Understanding these silent score killers is essential if you want to protect—or rebuild—your financial credibility.

One of the most common errors is incorrect personal information. A wrong PAN, mismatched address, or spelling error in your name can split your credit history into multiple profiles. When lenders pull your report, they may see incomplete or inconsistent data, lowering confidence and score—even if you’ve paid on time.

Another frequent issue is accounts shown as active even after closure. Many borrowers close loans or credit cards but never verify if the lender updated the status correctly. An account that should be marked “Closed” may still appear as “Open” or “Overdue,” continuously dragging down your score.

Duplicate loan entries are another silent killer. Sometimes the same loan appears twice—often due to data reporting errors during transfers between lenders or recovery agencies. This doubles your perceived debt and inflates utilization, hurting your score without you realizing why.

A particularly damaging error is incorrect repayment history. A single EMI wrongly marked as “late” can significantly reduce your score. Over time, repeated reporting mistakes compound the damage. Borrowers who always paid on time are often shocked to see red flags they never caused.

Settlement-related misreporting is also common. After a lawful settlement, some lenders incorrectly tag the account as “Written Off” instead of “Settled.” This distinction matters. “Written Off” signals abandonment, while “Settled” reflects a negotiated closure. Wrong tagging can extend the negative impact far longer than necessary.

Common CIBIL errors borrowers overlook include:

- Wrong PAN, name, or address details

- Closed accounts still marked active

- Duplicate loan or credit card entries

- Incorrect late payment marks

- Wrong loan type or amount reported

- Settlement marked as “Written Off” instead of “Settled”

Another silent issue is high credit utilization caused by outdated limits. If a lender fails to update your reduced balance or increased limit, your utilization ratio looks worse than it actually is—pulling your score down despite responsible use.

The danger of these errors is not just the score drop—it’s the lost time. Borrowers often spend months trying to “behave better” financially, unaware that the real problem is data accuracy. Without correction, improvement efforts show little result.

So what should borrowers do?

Start by checking your CIBIL report regularly—at least once every 3–6 months. Look beyond the score. Verify each account, date, amount, and status. If you spot an error, raise a dispute immediately and follow up until it’s corrected. Keep documentation like NOCs, settlement letters, and payment proofs ready.

This is where Lawfully Finance adds real value. Beyond debt relief and settlement, Lawfully Finance helps borrowers audit their credit reports, identify hidden errors, and guide disputes correctly—ensuring your report reflects the truth, not mistakes.

Final Thought

Your CIBIL score shouldn’t suffer because of errors you never made. Silent score killers thrive on inattention. Awareness, verification, and timely correction can restore control and open doors again.

👉 If you suspect errors are hurting your CIBIL score—or want expert help fixing them—take the next step with Lawfully Finance:

https://lawfullyfinance.com/step/sign-up/